The energy crisis and the international context have plunged many households into financial difficulties. Some owners are no longer able to meet the deadlines of their mortgage and quickly find themselves excluded from the banking system. To respond to the distress of these owners who risk losing their property, real estate and finance professionals have brought up to date a very old real estate transaction, the sale with repurchase.

A response to the rigidity of banks

La sale for repurchase is intended for owners who are unable to obtain bank financing and who are in urgent need of funds. These may be badly indebted individuals who have taken out too much consumer credit and are struggling to make ends meet. It can also be entrepreneurs who want to unlock cash for their business. They find themselves without a solution to move forward with their projects because the banks refuse to grant them a mortgage loan.

With the standards of HCSF (High Council for Financial Stability), the conditions for obtaining a loan are increasingly strict. Your monthly payments should not exceed 35% of your income. Banks have the right to derogate from this rule, but only on a few files per year. In addition to the HCSF, the selection criteria remain very unfavorable to entrepreneurs, retirees, fixed-term contracts, etc. This rigid policy of granting loans aimed at protecting borrowers proves to be harmful for many owners. Despite the provision of collateral for real estate, banks refuse to lend to owners who do not tick all the usual boxes. Unlike Anglo-Saxon banks, French financial organizations do not lend solely on the value of real estate. They attach more importance to the professional situation of the borrower than to the quality of the property.

What is the principle of a repurchase sale?

To avoid these banking constraints and succeed in freeing up cash, financing specialists have reintroduced into practice an old transaction called a repurchase sale. The sale with repurchase would have been practiced as of the Middle Ages. The word “réméré” comes from the Latin “redimere” which means to redeem. The repurchase sale is defined by articles 1659 to 1673 of the Civil Code. It was renamed sale with right of redemption in 2009. Some companies speak of real estate portage, but the principle remains the same.

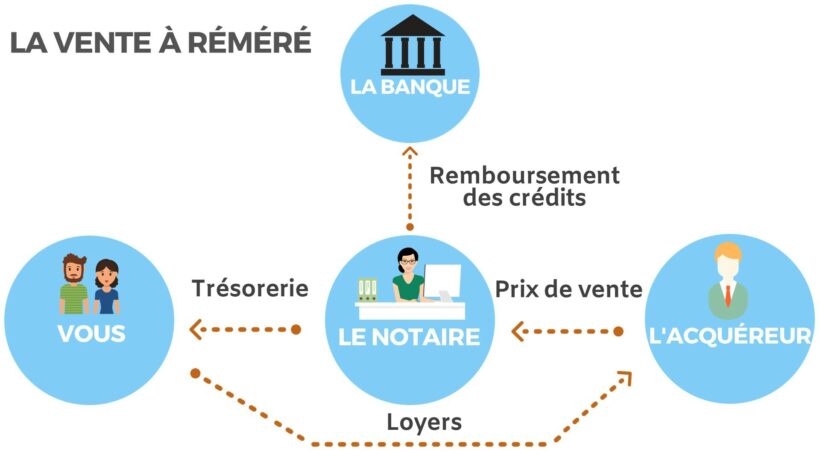

During a repurchase sale, you sell your property while continuing to occupy it with the possibility of buying it back or reselling it at any time within the limit of five years. The seller receives funds through the sale of his property. He can use them to repay loans or finance a project. After the sale, the seller continues to enjoy the property. He can very well rent it out and collect the rents. As soon as he wishes, he has the possibility of buying back the property at a repurchase price defined at the start. The maximum duration to redeem the property is defined by the civil code at five years.

As with any real estate sale, the sale contract for repurchase is a notarial deed. A notary's office is responsible for instructing the transaction and drafting the deed of sale which includes the specific clauses of the operation. The notary's office exercises its duty to advise by warning the seller about the sale price, which is lower than the market value.

The advantages and dangers of a repurchase sale?

The repurchase sale is a last resort solution to release cash without going through a bank. The sale of the property is used to settle loans, finance the purchase of a new property or solve the cash flow problems of a company.

One of the advantages of the repurchase sale is the notary fees on redemption which are 1,5% against 7,5% for a traditional sale. The redemption is not a new sale but a cancellation of the initial sale. The sale price for repurchase is below the market value of the property.

To carry out this transaction, you must first find a buyer who will want to buy your property for redemption. In return for occupying the property, the seller pays rent after the sale. To remunerate the buyer, the purchase price is often higher than the sale price. For example, a property with a real value of €300 is sold for redemption at a price of €000 to an investor who becomes the full owner of the property. If the seller is over-indebted, he settles his credits thanks to the proceeds of the sale and becomes eligible for bank financing again. After the sale, the seller remains in the property by paying compensation similar to the amount of rent. He can redeem the property at any time for €200. If he cannot or does not wish to buy back the property, he has the option of reselling it at the market price (€000) and collecting €215.

The interest of the operation is to succeed in freeing up funds by selling a property while keeping the enjoyment of the property for a certain time. If you were in default on your home loan, the bank is automatically reimbursed through the sale of the property. The repurchase sale is also a means of putting an end to a banking dispute and avoiding a property foreclosure procedure.

The real danger of a repurchase sale is not being able to redeem the property within the time limit. To avoid this unfavorable outcome, it is imperative to anticipate the exit by buyout by determining beforehand its borrowing capacity. You can contact a broker who can determine your financing capacity. The sale with repurchase can be an excellent means of resolving a delicate financial situation on the condition of being well supervised. For several years, companies specializing in the realization of this assembly can help you, by finding the right buyer, to carry out this operation in the best conditions.